Africa’s Nature-Based Carbon Project Pipeline: Insights from CAPE

Africa has a significant nature-based carbon project pipeline – and a clear gap between potential and investment readiness. When FSD Africa, Finance Earth and ANCA assessed 149 projects through CAPE’s first cohort pipeline process, the data pointed to more than 1.6 billion potential carbon credits, at least US$48 million in pre-implementation financing needs, and strong participation from Africa-headquartered developers. It also showed that most projects need more than capital; they need the technical, commercial and governance foundations to convert early market interest into formal commitments.

Nature-based carbon projects are increasingly recognised as a key component of Africa’s climate mitigation and adaptation strategies. Across the continent, project developers are working to restore landscapes, protect ecosystems, strengthen livelihoods and generate high-integrity carbon credits. However, these efforts can face persistent challenges in accessing the capital, technical support and market connections required to reach scale.

In order to cbridge the gap to get projects to investment close, FSD Africa, in partnership with Finance Earth and the African Natural Capital Alliance (ANCA), launched the Carbon Accelerator Programme for the Environment (CAPE) in 2024 to catalyse investment into high-integrity and high-impact nature-based carbon projects across Africa by offering project development and transaction advisory support.

As we open CAPE’s second Expression of Interest (EOI) for projects across Africa, we’re sharing key insights from the first pipeline assessment. These findings can help investors, buyers, project developers and wider market actors understand where opportunities are emerging, and where additional support may help the market to scale with integrity.

Pipeline assessment: 149 applications across Africa

In CAPE’s first round, we received 149 applications across a wide range of projects and geographies. This included 105 applications for an Africa-wide EOI and 44 applications through a specific EOI process targeted at Ethiopian projects.

Projects were assessed through a staged process designed to understand project eligibility, development status, impact potential and alignment with CAPE’s support model. The assessment considered whether projects were aligned with CAPE’s focus on nature-based carbon, whether carbon revenues formed a clear part of the investment case, and whether investment readiness support provided through CAPE would be additional at the project’s current stage of development.

CAPE engaged projects at a range of development and investment-readiness stages. Some projects had completed feasibility work, started developing a Project Design Document (PDD), and had begun engaging buyers or investors. Others were still building important foundations, including feasibility studies, baseline assessments, community engagement, legal structuring or carbon revenue strategy.

This range does not translate to a lack of quality or ambition in the pipeline. Rather, it reflects the reality that projects require different forms of support at different points in their development journey. Some projects may be well placed for transaction advisory now. Others may have strong long-term potential, but require earlier-stage support before engaging buyers, investors or carbon market counterparties in detail.

Through this process we were able to select seven projects to receive tailored CAPE support, bespoke to their development stage and individual needs.

What our analysis shows

Africa’s carbon market opportunity is significant. The African Carbon Markets Initiative (ACMI) estimates that there is the potential to generate 2.4 billion Verified Carbon Units (VCUs) across Africa by 2030. However, nature-based carbon market remains nascent despite Africa’s significant potential. According to ACMI, 50 million VCUs were issued and 25 million VCUs were retired across the continent in 2024. African carbon projects have so far only captured 16% of the global market.

The range and scale of projects assessed by CAPE points to the magnitude of this opportunity, and how barriers can be overcome to unlock Africa’s carbon investment potential. The 149 applications assessed presented:

- an approximately 3 million hectares of land;

- more than 6 billion potential carbon credits or tonnes of CO₂e over project lifetimes;

- at least US$48 million in identified pre-implementation financing needs; and

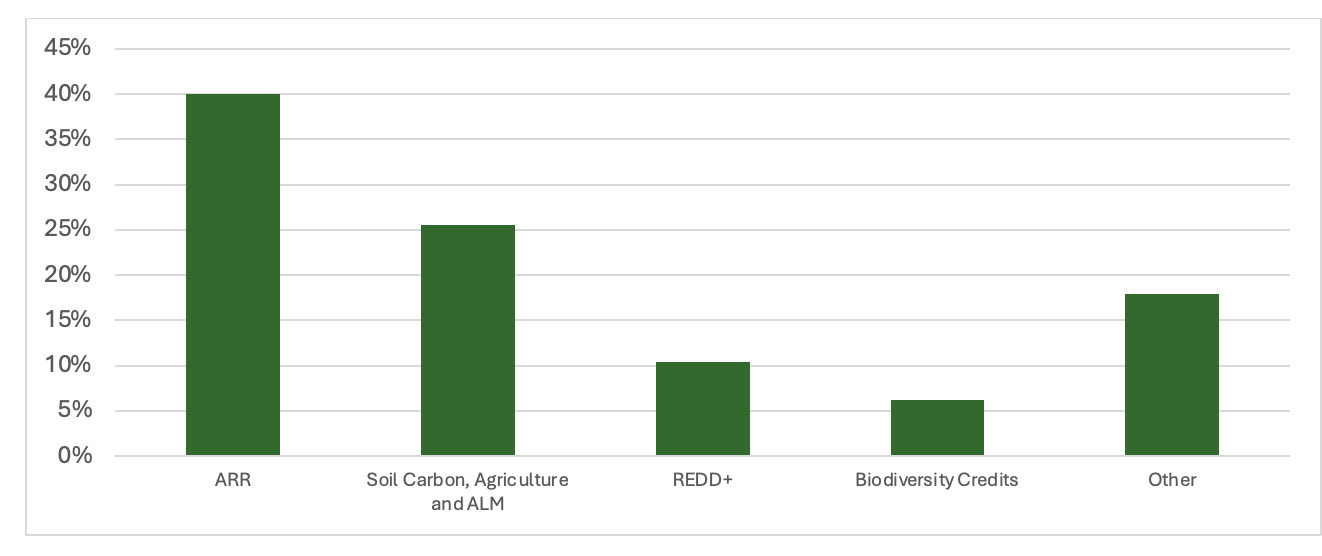

- a wide spread of project types, including Afforestation, Reforestation, and Revegetation (ARR), agriculture and agricultural land management, soil carbon, REDD+, blue carbon and wetlands, biodiversity, biochar, bioeconomy, rangelands management, agroforestry and other landscape-scale approaches.

Chart 1. Type of projects applying to CAPE’s first cohort, % of total

For buyers and investors, the opportunity is not only the volume of potential credits. The more important question is what development stage projects have reached, and how these projects can transition from design to delivery and still deliver high quality and impactful credits.

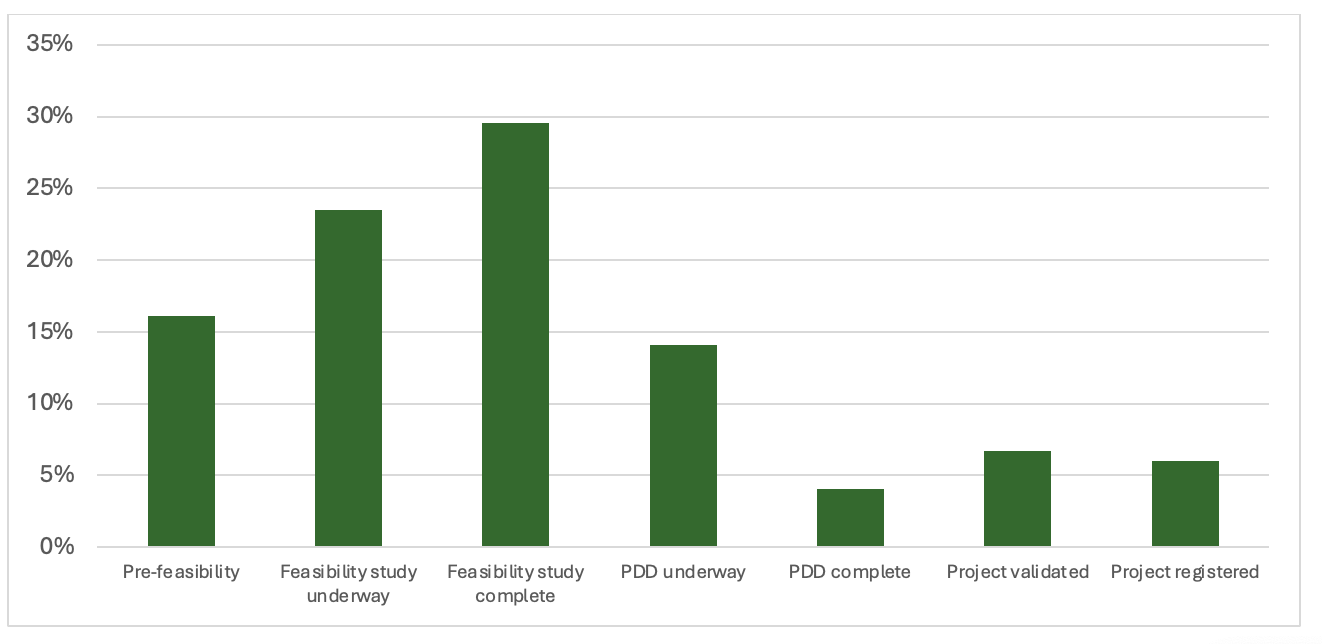

The readiness gap

For carbon projects, completing a feasibility study is a major milestone towards investment readiness. A feasibility study transforms a carbon project from a concept into a credible investment proposition by testing whether a project can generate additional carbon benefit, stress testing the proposed approach for monitoring, reporting and verification (MRV), securing initial stakeholder consent and input, and producing the initial financial modelling for the project. Post-feasibility projects must then complete a Project Design Document (PDD); the definitive technical and procedural map of how a carbon project will generate, measure, and verify its credits, and is critical for achieving validation by a carbon standard.

About 39% of CAPE applications had not yet completed their feasibility study, which can cost over US$70,000 to complete, while around 44% had completed their feasibility study but not their PDD. Their identified needs reflected this, with projects seeking support with investor engagement, development of MRV systems, benefit-sharing frameworks, legal support, financial modelling, and PDD development.

This demonstrated that while many African carbon projects are not starting from zero, there is a clear readiness gap to proving post project feasibility, progressing to PDD stage and accessing investment for implementation. This is a critical insight for the market. Many projects are not only looking for delivery funding. They also often require deep technical, commercial and governance foundational support.

Chart 2. Project development status of CAPE Applicant projects, % of total

Buyer and investor engagement

To unlock delivery, projects seek investor or carbon buyer engagement to secure funding and purchase commitments. Through CAPE’s first round of project assessments, we identified a clear gap between early buyer and investor engagement and formal commitments.

While 69% of projects had engaged with investors, only 10% had executed financing agreements. Similarly, 62% had spoken with buyers, but only 12% had progressed to formal arrangements, such as MOUs or Heads of Terms.

Market interest exists, but many projects require further work before this interest can convert into Heads of Terms, investment, or offtake arrangements. Buyers and investors often require greater confidence on methodology selection, expected credit volumes, delivery risk, community engagement, legal structures, benefit-sharing arrangements, regulatory considerations and long-term project governance.

For developers, preparing this information can be resource-intensive, particularly before carbon revenues begin. Introductions alone are unlikely to be enough; projects also need the documentation, analysis and structures required to move from early conversations into due diligence and, where appropriate, commercial terms. This points to another practical support gap in the market that CAPE is helping to bridge.

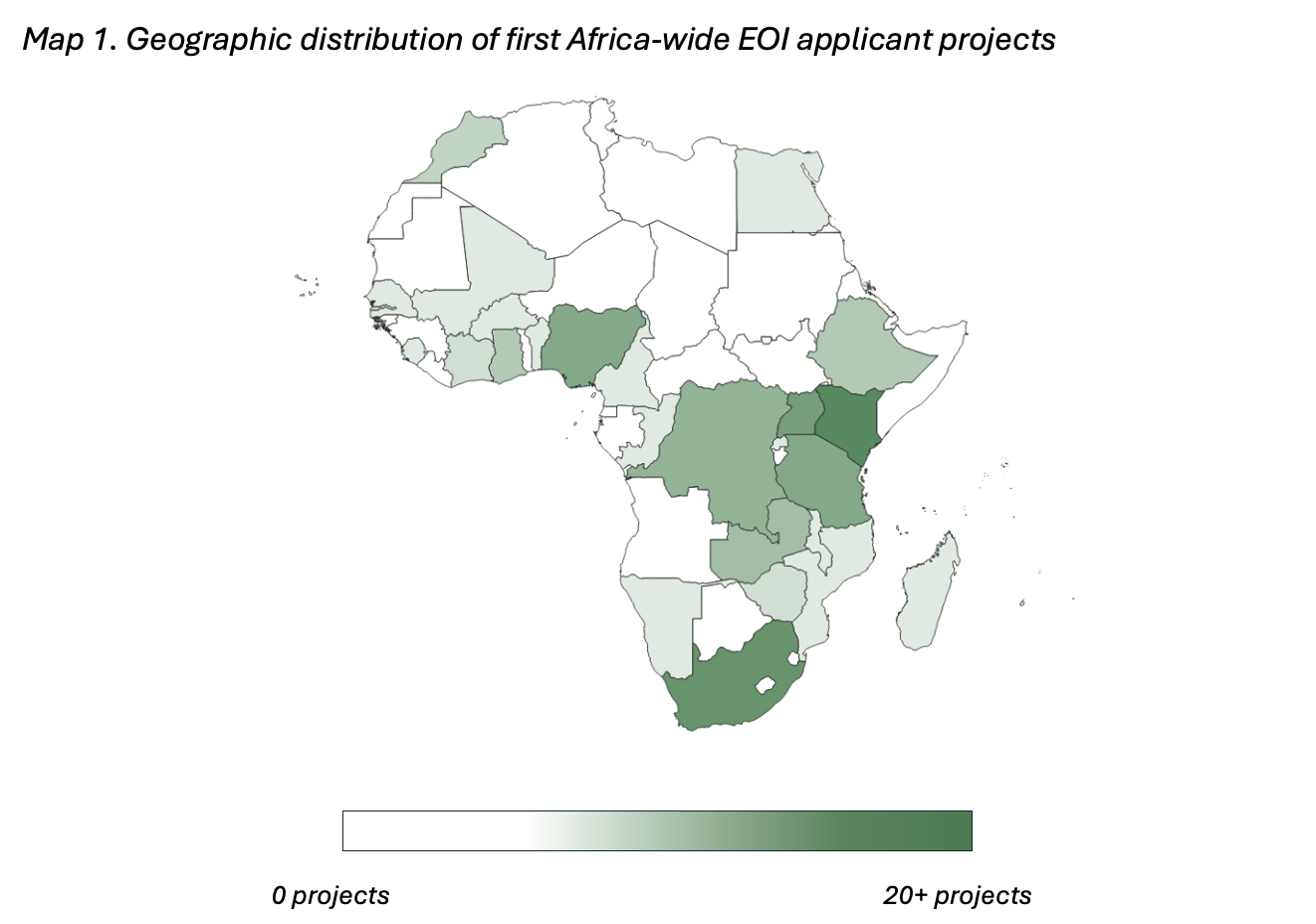

Geographic spread

Our assessment process demonstrates how Africa’s carbon projects are concentrated in key areas.

The 105 applicants to the Africa-wide EOI spanned 28 countries, with the highest proportions in Kenya (24%), South Africa (13%), Uganda (9%) and Nigeria (7%). Our Ethiopia process, covering 44 projects, provided visibility into the Ethiopian market.

For investors, this concentration is a useful signal: the leading markets are also among the jurisdictions moving fastest to formalise carbon-market regulation, host-country approval pathways and Article 6 frameworks, which can reduce regulatory uncertainty and strengthen confidence in eventual credit issuance. On the other hand, this distribution demonstrates how progress is uneven across the continent.

Africa-headquartered developers

We found that Africa-headquartered developers are strongly represented, demonstrating local ownership and leadership, but also distinct capacity-building needs.

In the first Africa-wide EOI, ~71% of project developers were headquartered in Africa. In the Ethiopia EOI, ~82% of applicants were headquartered in Africa. Clearly, Africa-headquartered developers are already a major part of the nature-based carbon project pipeline. Many Africa-headquartered developers are close to the landscapes, communities and local delivery conditions these projects depend on.

However, based on applications received, they tended to be earlier in their carbon project development journey, with less access to early funding, technical support, legal advice and buyer networks. Early support could help more Africa-headquartered developers move from promising project ideas to investable opportunities, enabling them to capture a greater share of the market.

This is a balance that CAPE is working to navigate: supporting African-led project development, while also selecting projects that can realistically move towards investment readiness within programme timelines. We look to draw on the learnings to date, to ensure earlier-stage Africa-led developers have a genuine pathway into the programme and through it.

What this means for the market

CAPE’s first 149 applications illustrate that Africa has a significant nature-based carbon project pipeline, with broad landscape coverage, projected credit potential, diverse project types and strong participation from Africa-headquartered developers.

The same data also shows that pipeline volume alone is not enough. The market gap is increasingly about readiness and buyer and investor conversion: helping projects move from projected carbon potential and early market interest towards buyer and investor diligence, formal commitments, implementation and, ultimately, credit issuance.

As we launch CAPE’s second EOI process, these insights are already shaping how we think about project selection and support. Applications are now open for high-integrity, high-impact nature-based carbon projects across Africa seeking patient capital for project development, transaction support and buyer and investor engagement.

Future Living Lab posts will share further practical lessons from CAPE’s work with project developers, buyers, investors and other market actors.